What is Bitcoin and how do we define trust?

Bitcoin, anonymously created by Satoshi Nakamoto, is a technological software network of nodes which enable the transference and velocity of coins called bitcoins via clever usage of double SHA256 cryptography and a network consensus mechanism known as Proof of Work. Being decentralized and supposedly trust-less in nature, it is a puzzlement as to how this system operates and sustains itself with no centralized entity, after all at the end of the day it is individual people using this open source software for their own individual needs. Today, the answer is easy to see after 13 years of network growth; network participants banded together to create centralized and decentralized exchanges, trading platforms and counter-parties to further fuel Bitcoin adoption and usability. What remains unclear is, how vital of a role do these Bitcoin trading platform participants play in the overall exchange operations, and what are the implications of trusting these participants? Perhaps through social network analysis we can detect the most at risk centralized entity in case of security incidents to prevent critical damage.

Diving deeper

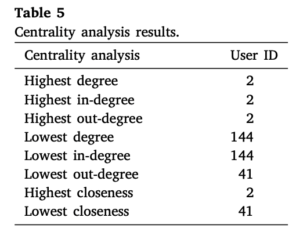

In May 2022, researchers performed a social network analysis of BTC-Alpha, a Bitcoin trading platform. By taking the dataset(N=150) of user’s credit evaluated by Revain, a weighted trust of the network participants is gauged as a graph and visualized below using Gephi:

Here, the nodes correspond to the unique user ID and the largeness and shade of red (left color bar) implying higher node degree. The right color bar at the bottom of the figure corresponds to the edges where white implies lowest weight between nodes and purple implies the highest.

From this graph, it is possible to further derive data on node degree, closeness and betweenness. As they found in their Table 5 results below, user 2 seems to be the most trusted person, having the most degrees on top of the most IN and OUT degrees. Of course, it is important to note that past trust is not indicative of a guaranteed future of continued trust, but for the purposes of this analysis we simplify trust to be merely the centralized entity node(s) who are connected to majority nodes. From this, it is clear the influence user 2 has over the whole network, as user 2 interacts with and keeps track of an array of network participants any of whom it can quickly connect with. Inversely, user 144 would find it hardest to spread roots in the network due to the low degree and overall lack of trust.

In terms of closeness, that is the shortest path between all nodes, we find user 2 once again being most influential and having the power to affect the entire network the fastest. On the flip side, user 41 would deal the least damage, having the longest shortest path.

Lastly, betweenness analysis cements user 2’s vital role in filling otherwise bridge gaps in the graph, and hinting at it’s importance in the distribution of information and social communication. The ability to easily affect flow implies user 2 is most likely an Automated Market Maker (AMMs) which uses bots to facilitate buy/sell order-books or a large entity with a lot of authority. User 41 falls on the opposite spectrum having the least influence of any sort.

Conclusions

Through the use of social network analysis, we are able to better perceive the world in which we inhabit. With the existence of a network such as Bitcoin to counter our current Fiat network system, it must be imperative to understand the potential network effects that arise in this new system and the implications and revisions on the existing system due to this. By analyzing 150 users trading activity, researchers find the truth of the current Fiat Standard system, that is centralized entities enable the most flow and information transference with the best efficiency. The Federal Reserve and the various giga-banks across the globe are various examples of such centralized entities and in the global marketplace, their fundamental centralized role and the risks of their absence are further highlighted by this research.

Sources

Chang, Victor & Hall, Karl & Xu, Qianwen & Doan, Le Minh Thao & Wang, Zhi. (2022). A social network analysis of two networks: Adolescent school network and Bitcoin trader network. Decision Analytics Journal. 3. 100065. 10.1016/j.dajour.2022.100065.